http://paulgrignon.netfirms.com/MoneyasDebt/MAD2014/problem.htm

|

“Twice-Lent Money”

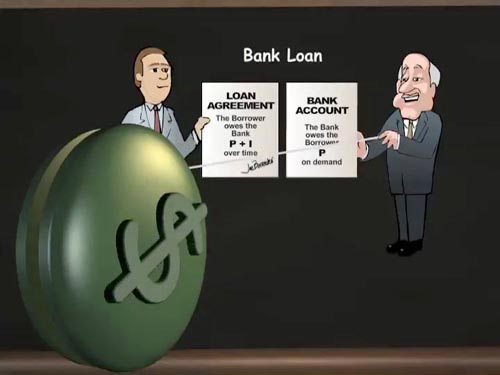

Summary Today, most money is created as debt on a schedule by a borrower borrowing it into existence from a bank or other depository institution. This money is spent and circulated until someone puts it aside as savings or lends it a second time as existing money. Either way, as long as the money remains saved or lent, the money originally created as a loan from the bank is not available to the borrower that created it, except as another loan. The original money creation loan will be have to be paid off with the Principal of some other loan, making repayment of that loan dependent on another loan’s Principal and so on, ad infinitum. Savings create an ongoing volume ofPerpetual Debt for as long as the volume of savings remains unavailable to be earned on time by the borrowers that created it. Animated Video: The amount of the Perpetual Debt can neither shrink nor slow down in its delivery without causing mathematically inevitable defaults. Therefore new borrowing from banks must never decrease or slow down. Otherwise people will lose their homes because of a mathematical shortage of Principal. Our money system is only functional when it is growing. It cannot handle shrinkage, or “de-growth” as some call it, without defaults. That makes it ill-suited even for normal economic mood swings which should be expected to be cyclical simply because everything in the Universe is cyclical. The question always asked by politicians and economists is “What causes the business cycle?” as if it should be prevented. I say it’s the wrong question. Accept the Business Cycle as natural and adapt to it. The question to ask is: A money system dependent on never ending growth is absolutely suicidal in a world already in next ~ Money is created as a promise to pay it back |

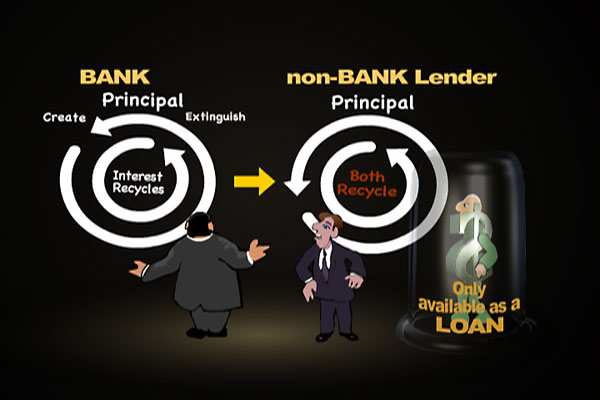

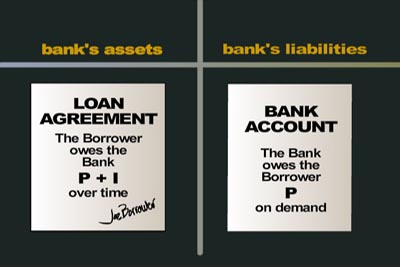

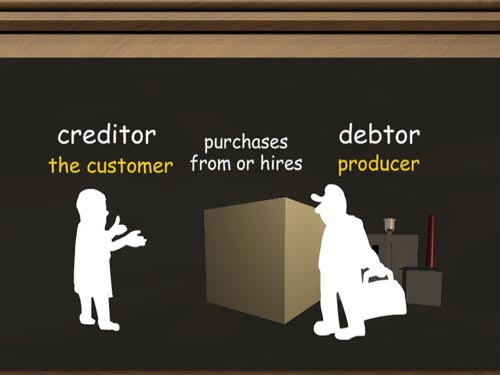

“Twice-Lent Money”page 2 “Twice-Lent Money”page 2Money is created as a promise to pay it back home / contact Today almost all of our so-called money supply is created as bank credit. The borrower creates bank credit (promises of fiat cash on demand), by signing a contract to pay fiat cash or bank credit money back to a chartered bank or trust. Thus, bank credit money is a promise of repayment in itself. So also is fiat cash, which is “real money” in the sense that it is legal tender. The courts enforce its acceptance. Legal tender is created by the nation’s central bank as a promise of repayment (usually by the national taxpayer but now other debt) that is not paid back, just serviced with perpetual interest. This debt creates the “base money” supply that provides the system with central bank balances and physical cash. But base money is often just 5% or less of the money supply. The rest of the money supply, the vast majority, is “retail” bank credit, numbers on computer screens, promises of repayment in bank credit, denominated in legal tender units. Most of this bank credit is created as mortgages, and must be paid back on time. I All of it is Money created as Debt. For those who would like to read a succinct written explanation, I have a one-page PDF: Here is a more detailed explanation of where money comes from: A 9-minute cartoon explains our money system and why it leads to collapses and bailouts And this is my full analysis and my movies which have gone around the world and are online in at least 24 languages. Money as Debt III – Evolution Beyond Money back / next ~ Interest is not the mathematical problem some people think it is |

| “Twice-Lent Money” page 3 Interest is not the mathematical problem some people think it is home / contact Banks charge interest (I) which means that the total amount of money the so-called borrower (actual money creator) must pay the bank exceeds the Principal amount (P) created. This is represented by the inequality P < (P + I). This leads many people to believe that interest is the fundamental problem that makes the economic system mathematically unstable because “obviously” there isn’t enough money created to pay both Principal and Interest. The many variations of this stranded on a desert island fable purport to prove that interest is mathematically impossible to pay from the original principal alone. Please follow this link if you continue to believe this misconception.

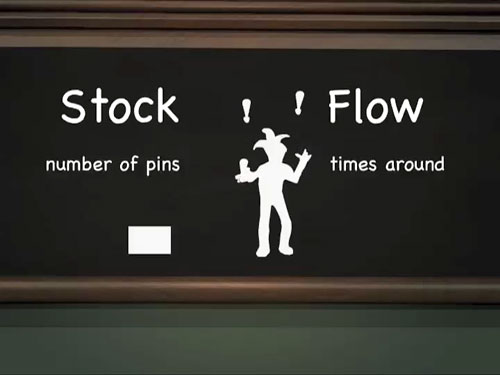

The chapter on Interest from Money as Debt III Here is an animated demonstration illustrating how a total of $1100 Principal + Interest can be paid back to the bank with just the original $550 Principal. Flow multiplies stock. • The green line indicates the bank spending the interest back into circulation. This is the flow that allows the same money to be earned and paid again and again. • The red flash is Principal being extinguished upon repayment to the bank.

RIgorous Attempt Proves Only the Obvious

They failed to prove anything but the obvious fact that UNPAID loans at interest grow exponentially. Fortunately, the authors and I are in agreement that we need to move away from the concept of money as a “quantity”, a thing-in-itself. The “medium of exchange” can be replaced by a “means of exchange”. |

|

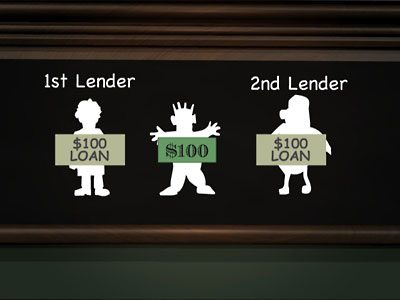

“Twice-Lent Money” page 4 I claim there is a very simple mathematical proof of an inevitable cause of system collapse due to income disparity that builds up – even if all debts are PAID. This can happen in a complete absence of monetary interest. That cause is our concept of money as a thing-in-itself in finite supply. Money can be lent more than once creating mathematically inevitable defaults if the demand for, or supply of, new loans diminishes. This is especially true when that thing-in-itself only enters circulation as debt, a promise of repayment in itself, which is what money is today. What does it mean for money to be” twice-lent”? It’s very simple. 1. lent again indefinitely to banks as the savings of depositors; 2. lent again indefinitely by depositors through money market funds offered by banks;. 3. lent again indefinitely by depositors privately. If all money were created this way, is it not clear that, for the borrowers to pay off their loans on time, the depositors must spend their deposits so the borrowers can earn them on time? As long as the borrowers’ debt, which is now the depositors’ money, remains lent to anyone… bank, money market fund, private lending, whatever, if it is LENT not SPENT, the only money available to be earned by the original borrowers to pay off the original debt will be Principal already commited to another loan. As a society, we are caught between lenders. This trap is invisible to us because we all, public, politicians and economists alike, ignore the fact that money is created as a debt cycle. We fail to see that when money is created as debt, savings put us in the position of owing the same money to two or more lenders simultaneously. As a society, and invisible to us, we avoid default by borrowing from one to pay the other and vice versa.

This works just fine when the amount involved is stable or increasing. But… whenever a lender won’t lend the full amount on time, or whenever the demand for money-creating bank loans slows down, for any reason, including natural cycles, someone must default. When a lot of people default it’s a crash. Imagine that 75% of all money created is perpetually unavailable except as a loan. Therefore, assuming the original borrower earns P and pays it back to the bank that created it, the original borrower had to use 0.75 P from someone else’s P that they owe to a lender. So now that loan is short 0.75 P. The original Principal Debt has been paid off with either: This leaves those loans without the 0.75 P needed to pay them. Existing money must be lent or new money created to avoid default. Either way the next debt is short 0.75 P. We now have an ongoing dependence on the amount of 0.75 P never decreasing, and its delivery by the banking system as new money never slowing down. Otherwise default is inevitable. Now, so far I have only mentioned a second debt of the same money. But there is no limit to how many times the same money can be lent in series making an unknown and perhaps unknowable number of loans dependent on the same Principal. If that number of loans in series were N then any shortage of new P could potentially be multiplied by N, causing multiple defaults of the same Principal ( NP ).

The Perpetual Debt Level is the total amount of money created that is not available to pay off the debt that created it, without creating a new debt. And, in the real world, amazingly enough, no one in economics that I know of has yet conceived of, much less tried to determine, the level of Perpetual Debt. And so far my repeated challenges to economists to refute the simple logic presented above continue to go unanswered. I was invited to write a paper, which I did, but nothing so far has come of it. My paper published by the World Economics Association: “Proposed new metric: The Perpetual Debt Level” |

“Twice-Lent Money” page 5

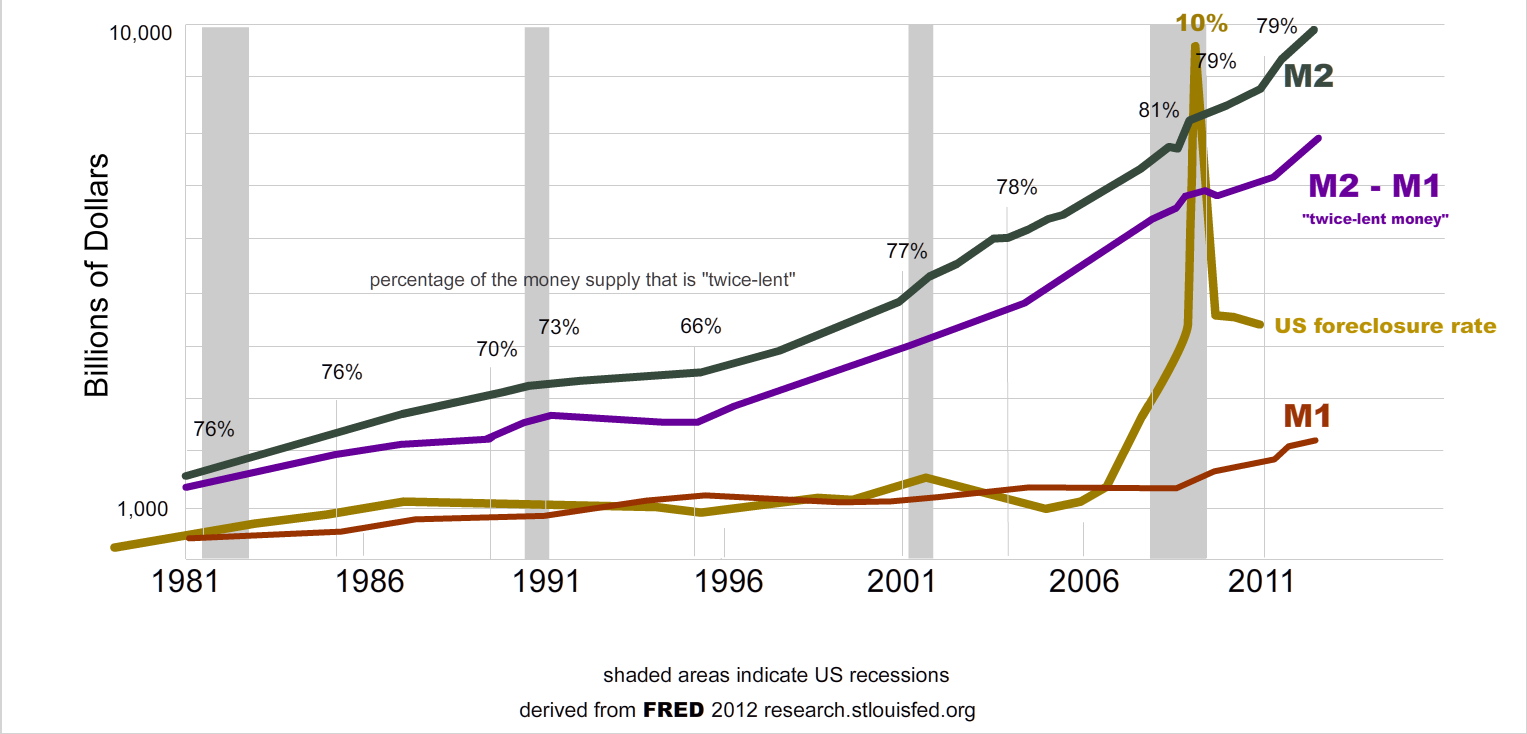

M2 minus M1 is “Twice-lent Money”

home / contact

| Definition of ‘M2’ from Investopedia

A measure of money supply that includes cash and checking deposits (M1) as well as near money. “Near money” in M2 includes savings deposits, money market mutual funds and other time deposits, which are less liquid and not as suitable as exchange mediums but can be quickly converted into cash or checking deposits. |

From the definition quoted above, it follows that M2 minus M1 excludes the cash and various forms of checking accounts that constitute M1 and leaves only savings deposits, money market mutual funds and other time deposits.

Therefore, we can conclude that M2 minus M1 is a proven ongoing volume of money that was created as one debt and is now either not available or only available as a second loan of itself. What are the consequences when this volume increases or decreases?

According to the chart below, bank savings normally constitute about 75% of M2. The recent crisis happened when bank savings hit81% of M2. During the booming 90’s, bank savings dropped as low as 66% of M2. Is there a rational cause and effect here?

On the graph below, the green line (savings plus cash & checking) rises steadily while the red line (cash & checking) rises and falls.Whenever the proportion of M2 that is savings (twice-lent money) increases for four years or more, a recession and foreclosures have followed. This is only logical once we realize that savings are an interruption of debt cycles. The increase in savings means areduced supply of money available to be earned by borrowers without someone incurring another debt. If that debt is not incurred and the savings remain locked up, someone must default due to an actual shortage of available Principal.

US Money Supply

click on image for larger version

And that’s not the end of the possible damage that could be caused by a perfectly natural slowdown in the demand for bank credit.

This graph only shows where the money was at that moment, in the banking system. It provides no information about how many private debts (N) might have been incurred on the way to it being deposited. In the case of N debts, any shortage of new bank-created Principal would be multiplied by N in resulting defaults.

On the other hand, there are mitigating factors such as ever growing government debt, rolling credit, interest-only mortgages, credit cards and banks creating debt-money to buy equities that put new money into the system that doesn’t have to be paid back on a schedule. But the last three are pro-cyclical, meaning they shrink just when they are needed to expand. Only astronomically increasing government debt staved off collapse in the 2008 crisis (bailout). In Cyprus, the banks simply negated some of the banks’ debts to their depositors (bail-in)

The full animated graphical explanation.

|

Solution:page 1 The solution to the problem is to expand the concept of money to include Movie: Two Kinds of Money (6:53)

Two Kinds of Money1.The Scarcity Model: A single uniform quantity in limited supply made valuable by its own scarcity. 2. The Abundance Model. A promise of something specific from someone specific made valuable by its redemption in real production. The value of this type of money is defined by the promised redemption in goods and/or services. As such, this type of money is promises of an indefinite number of non-uniform commodities in indefinite supply and, unlike the limited quantity “coin” concept of money, the total quantity of these credits in circulation does not affect their value, because the value of a credit is defined by what its issuer will redeem it for in real goods and/or services. Examples are: business-to-business barter credits, customer rewards, travel points, discount coupons, mutual credit systems. E.C. Riegel was a passionate advocate of the abundance model. |

||

| “Twice-Lent Money” page 6 Who has these savings? home / contact

As the article above points out, corporations are sitting on mountains of savings that they won’t invest in production because there’s no demand. And there’s no demand because the money is now locked up in corporate savings, thanks to offshoring the manufacturing work to cheap labor countries. These company execs must somehow expect the people they threw away at home to go further into debt forever to buy their output. Henry Ford must be rolling in his grave.

But it goes beyond the corporations and today’s situation. It’s really about the design of the system. Savings are Perpetual Debt. The fundamental problem is the mathematical structure of money as a thing-in-itself in finite supply. All that is required to create mathematically inevitable defaults and collapse is income disparity. And Perpetual Debt has always been a dynamic within the money supply. In the past, gold coins accumulated in the hands of the economically powerful and only entered circulation as debt just as bank credit does today. Whole societies found themselves trapped in borrow from Peter to pay Paul and vice versa traps created by rich moneylenders. The same would happen to Bitcoin if it became the world’s currency. That is because its founding principle, |

Solution:page 2

The Essence of Money

home / contact

Movie: The Essence of Money, a Medieval Tale(7:36)

This short animated cartoon illustrates how the principle of the abundance model was used in medieval trade fairs to overcome any shortage of coins.

Market money was created from merchant IOU’s, dependable promises of merchandise or services direct from the suppliers of that merchandise or service. Credits for products and services were denominated in coin value as the measuring unit that everyone understood and in which prices were already set.

This simple invention freed the markets from the tyranny of the “quantity and ownership of money” because anyone selling something in reliable demand could spend their credits in advance of selling their products. These coin-denominated credits could circulate among third parties as if they were coins, facilitating any number of trades, until finally redeemed for the product or service promised by its Issuer.

The silver coin as the commonly understood and agreed upon unit of value was essential to the system, but the actual silver coins were not. The potential quantity of silver-denominated IOU’s was only limited by the actual production, trust and demand that gave them value.

The Essence of Money is the short that precedes Money as Debt III – Evolution Beyond Money, a detailed proposal of how the same abundance model of money, which I now like to call Producer Credits, could be applied today to create a truly liberated global money system.

Clearly the concept is not new, and in fact it has always been with us. According to the report linked to below, it is estimated that at least 20% of world trade is currently carried out using business-to-business barter or as the report refers to them, “capacity credits”. This report is a valuable read. The banks are being advised to get into the Producer Credit brokerage business as the authors believe this to be the liquidity of the future.

Capacity Trade and Credit: Emerging Architectures for Commerce and Money

back / next ~ An Economist’s Review

|

Grignon’s plan is available in summary form in its own must-see animated video. It appears to be a way of simultaneously overcoming both Say’s Law and the problems of the Bartercard concept. From the standpoint of scholars of the evolution of Keynes’s General Theory of Employment, Interest and Money, Grignon’s proposal amounts to using modern technology to replace an ‘entrepreneur economy’ with a ‘co-operative economy’ (see Keynes’s Collected Works, Vol. XXIX, pp. 77-80). This is because workers and other suppliers of inputs used by a company accept payment for their inputs in the form of claims on the output to whose production they have contributed. Since they cannot be sure what they can exchange these claims for in terms of claims on outputs of other firms, they are sharing the risk of the business with the owners of the business.” “…I find Grignon’s Digital Coin proposal especially well thought out. The time for this self-issued credit system to be implemented seems ripe both because of the failure of the existing bank-credit system and because we now have the technology to make it work.” |

||

“…the obvious solution is not merely to foster the use of transferable product-specific vouchers as stores of value but to make them company-specific and include expiry dates on them. Businesses that issue them could then be confident about the level of sales they can achieve before the end of the expiry period. This is where we go, roughly speaking, if we follow the ingenious Digital Coin proposal of Paul Grignon, a Canadian film maker whose excellent animated documentary Money as Debt deserves to be screened to all students of economics.

“…the obvious solution is not merely to foster the use of transferable product-specific vouchers as stores of value but to make them company-specific and include expiry dates on them. Businesses that issue them could then be confident about the level of sales they can achieve before the end of the expiry period. This is where we go, roughly speaking, if we follow the ingenious Digital Coin proposal of Paul Grignon, a Canadian film maker whose excellent animated documentary Money as Debt deserves to be screened to all students of economics.|

Solution page 4:

In this proposed system, Producer Credits are time-limited contracts for delivery of something specific from someone specific called the Issuer. For example, Toyota credits would be spent by Toyota to build Toyota products. Toyota’s employees and suppliers would be paid in Toyota Credits and spend them as money into general circulation. Acceptance of Toyota Credits would be very nearly universal so they could flow as money around the globe. Between the time that Toyota spends its Producer Credits on wages, plant and supplies, and the time the customers redeem them for Toyota products, (which might be a full year), these credits can be used as defined-value redeemable money by third parties not related to either Toyota or the final customer. Toyota would offer a discount on its products if they are bought with Toyota credits. Like interest, this discount would build over time from issuance, peaking at the maturity date which Toyota would set to match the time it wants to sell the products. Toyota’s customers would seek to obtain as much “money” in mature Toyota Credits as possible in order to get the best price. After maturity comes a grace period when Toyota Credits would still be redeemed by Toyota but could no longer be traded as money within the system. Unredeemed credits would expire after the grace period. The value of a Producer Credit is defined by the Issuer’s promised redemption in real goods and services and thus by the prices the Issuer sets. A Producer Credit must be also be backed by conversion to a shareholder claim on the Issuer’s equity in liquidation should the Issuer fail. In this way, “money” is created by a promise of production

The chapters on Self-Issued Credit from Money as Debt III A Producer Credit is a form of stock in the Issuer, in which the Issuer guarantees to buy back the stock with product or service. A dividend may be offered by the Issuer so that the redemption value rises to a fixed maximum at maturity. This dividend payment is promised in the form of additional product or service ONLY, which in practice will mean a lower price for the redeemer. Simply put, the Issuer honors its own Credits at a higher value (of its own choosing) than any other Issuer’s Credits. From the customer’s point of view, acquiring the Issuer’s credits earns a discount from the “regular price”. From the issuer’s point of view the “discount price” is the regular price. Ideally, all of the Issuer’s production will be bought with all of the Issuer’s own Credits that were spent to produce it. This is adapted from the principle governing consumer-producer cooperation in existence today. The essence of the idea is that, if a customer gives a farmer money for carrots in April, that customer gets more carrots than someone who just shows up to pay for the farmer’s carrots in September. This is deserved because the April customer has made a commitment and taken a risk on that particular farmer, as the price and quality of the carrots is not guaranteed, only the “share of the harvest”. Thus the April customer is an investor not a lender and the benefit derived is a dividend, no matter how it is calculated. An Issuer’s employees and suppliers are the first to give value in exchange for the Issuer’s Producer Credits. Then the Credits are spent at retailers and paid to other suppliers and employees. Some are put aside as savings and exchanged for newer Credits when they approach maturity.

The chapter on Savings from Money as Debt III Ultimately the customer that redeems the product gets the discount, not the employee that first accepted it. That makes it different than a particular person financing a particular farmer. However, to the extent that the “imaginary” discount at every level of Credit redemption is realized in lower retail price levels, everyone would realize the “discount” whenever they purchase anything. This concept of “money” makes it possible to monetize ALL goods and services in reliable demand.This seems to be, simultaneously, the most rational and most idealistic way to back a trading medium. Instead of backing currency with artificially valued gold, or with nebulous concepts of limited resource bases, this system very rationally backs the trading medium with the current and near future production of goods and services that produce the need for the trading medium. In addition, from an idealistic standpoint, the trading medium itself directly embodies the people’s faith in and support of each other. It should be noted that Producer Credits are also “money as debt”, but instead of being a debt of money itself, 1. the Issuer makes a sale and extinguishes its Producer Credits or; 2. the Issuer may replace expiring Producer Credits with new ones (roll over debt) or; 3. the Producer Credits expire, an immediate loss, leaving no legacy of debt. A Producer Credit is a contract for products and/or services and may be recorded either as an accounting entry or, in the future, encoded as a transferable digital object like a Bitcoin. But, rather than being a speculative commodity, this digital object would be a promise of a specific measure of goods or services. The Issuer would also guarantee redemption in product at par with the value unit. This creates a “floor” of guaranteed value. It is also possible to protect the value of Producer Credits from monetary inflation/deflation by being denominated in an inflation-proofed value unit. |

||

|

Solution page 5:

Those who have seen Money as Debt III – Evolution Beyond Money will see that the proposal for establishing a value unit presented below, differs significantly from the one shown in the movie and at the Digital Coin website. In Money as Debt III, I proposed a value unit that would be smoothly predictable by basing it on aweighted basket of national currencies, as many others, including the International Monetary Fund, do currently. My original proposal was to create this new unit by selling tradable “Perpetual Coins” for national currencies giving a Perpetual Coin a reliable redemption value in national currency, and, within the system, a differenttrading value defined according to a formula derived from national currencies, designed to be both a smooth curve and resist the general devaluation of fiat currencies. The important point to avoid getting confused about, is that Perpetual Coin was never to be like gold, a “single uniform commodity in limited supply”. Nor was it ever supposed to be a “reserve” of any sort. It was just an attempt to create a new unit for “value”, when the only value units people currently comprehend are their own national currencies (and in many places the US dollar). Ultimately the new Value Unit could be a simple formula that ensures that you always get back the same real purchasing power you put in, no more, no less. Therefore, I have come to the conclusion that money needs to be defined in terms of the things we need to buy with it and that this can be accomplished quite simply. While the list of necessities differs from culture to culture, place to place, and individual to individual, we can define, in the abstract, the quantity of everything we need or want to buy as Q. Therefore, whenever we make a purchase we compare the value to us of that particular purchase compared to the value of Q, which is all of the other choices for which we might need or want to exchange that amount of value. This leads to this current proposal which is that Producer Credits be valued according to the US Dollar value of a fixed basket of globally significant commodities which represent Q.

If this system were to be adopted, the composition of this basket would be forever a core topic of politics and economics. The one thing it can never contain is labor because real price increase is when prices of goods rise relative to the price of labor. However, at this time, and with no resources to create such an index, it is proposed to use the Rogers International Commodity Index, (RICI), which has a good reputation and its founder and namesake, Jim Rogers, is a wise man. The RICI basket tracks “futures contracts on 37 different exchange-traded physical commodities, quoted in five different currencies, listed on thirteen exchanges in six countries”.

The adoption of a common value unit by mutual agreement could be done right now by existing alternative systems of all kinds, even Bitcoin. It is simply a mathematical, logical and equitable route out of unstable national currency units and into a stable “common monetary language” as called for in the opening E.C. Riegel quotation. Monetary inflation/deflation of national currencies is filtered out by defining the value unit as the current national currency value of a fixed amount of real goods (Q). Defined this way, any form of money or credit can be made “inflation-proofed” while remaining translatable into any national currency via the foreign exchange market. back / next ~ Does this method of valuation create any distortion? |

|

Solution page 6:

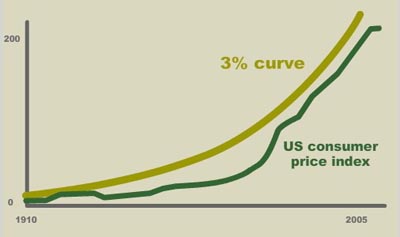

If the prices of all things rise more or less in proportion, that can be due to monetary inflation. More money has been created without a corresponding increase in real economic growth and the need for money. The powers-that-be actually target 1 to 3% inflation as a desirable policy. It’s a hidden form of tax on savers that accrues to governments and whoever borrows it into existence and spends it first. Three percent annual devaluation means that our money’s value is cut in half over a period of 25 years. The following chart adapted from data from the St. Louis Fed compares a mathematical 3% annual inflation curve with actual inflation in the USA from 1910 to 2005.

However, if oranges double in price due to freezing rain in Florida, that is not due to monetary inflation. So our system of valuation should filter out monetary inflation while responding to any real increase in the price of oranges. We start with the Rogers International Commodity Index (Wikipedia), the US-dollar value of a fixed basket of 38 world commodities that we shall use as our approximation of Q, the value of everything else to which we are comparing the value of our orange. If we choose to use 1000th of the Rogers International Commodity Index (RICI) as our definition, then our RICI unit could be $3.50 US at this moment in time. For arithmetic simplicity, let’s imagine these are exceptional oranges that currently sell for $3.50 US apiece. Therefore at this point in time, one orange costs one RICI. If, in future, due to national currency inflation, the value of the same fixed basket of commodities (the RICI index) rises to 5000, then one of our proposed RICI units is defined as $5.00 USD. If the price of oranges in USD has risen in proportion to everything else due to monetary inflation, then the formerly $3.50 USD orange must now be priced at $5.00 US which is 1 RICI. The RICI price of the orange hasn’t changed. If, due to national currency deflation, the index goes down to 2500, the price of an orange would be expected to drop proportionately to $2.50 US = 1 RICI. Again, the RICI price of the orange stays the same, immune from the fluctuations of national currencies. If the orange remains at the same price ($3.50 US) as before the deflation to 2500, then the orange hasincreased in price relative to the RICI basket of goods, which is a real price increase, not the result of monetary deflation. Its price is now 3.50/2.50 = 1.40 RICI. If the RICI increases to 4,000 and the orange increases in price to $5 USD, then that orange, priced in RICI is 5.00/4.00 = 1.25 RICI. Monetary fluctuations are filtered out, real price increases are not, precisely as would be expected. Thus we have a very simple means available right now to create an inflation-proofed value unit that any alternative money system can voluntarily adopt. All it takes is global agreement on a value unit to take the first step towards making disparate systems globally compatible. |

|

Solution page 7: 1. Selling Producer Credits for conventional money relieves the “twice-lent money” problem of the current system. Money that would have been tied up in savings and unavailable to the original borrower to earn, is, instead, spent on Producer Credits, which are investments in short term production. The bank credit is returned to circulation free of any second debt-of-itself and, theoretically at least, available to be earned by its original borrower. 2. Creation of the “money supply” would be by those who produce what we want to buy. ONLY those who produce what is reliably in demand get to spend credit before it is earned. This allows anyone with something in demand, including individuals, to spend their own self-issued credit with whomever will accept it. It is only to be expected that, because we pay taxes to governments and buy the products of large corporations, the Credits of governments and corporations would naturally predominate in general circulation. However, it would also be perfectly possible to have any number of limited circulations on a city, village or even personal basis voluntarily connected as we do now on a natural “tribes” basis through social media. 3. Efficient. Producer Credits must ultimately be spent on the Issuer’s product or become worthless. As well, Issuers would be required to provide the full purchasing power to absorb their full production. This would tend to favor a full clearing of production, leaving no wasteful unsold excess. 4. No legacy of debt. Money as Producer Credits would be mortal like all things in nature. Born from a promise that is either fulfilled or expires unfulfilled, Producer Credit money would not depend on indebting individuals, now or in the future. Unlike the current system which depends on a legacy of debt, this form of money creation could not, by itself, create one. 5. Inflation-proofed savings. Despite the temporary nature of Producer Credits, wealth could be stored in them indefinitely, insulated from monetary inflation/deflation. Producer Credits can be held until early maturity and then traded for newer Credits. This process of rolling over Producer Credit savings could be automated by brokerage services. Being viewed as a reliable Producer Credit for savings would be desirable to any Issuer. 6. Informative. The patterns of Producer Credit trading and saving would yield valuable predictive information about customer preferences, and confidence in Issuers, providing economists with useful work in reading this information and predicting the right course of action for Issuers. This information would be anonymous on the personal level. 7. Voluntary. Because all Producer Credits must be refused by default, acceptance would always bevoluntary. It would be possible for anyone to refuse to accept payment in any particular Issuer’s Producer Credits. This provides the general populace with an additonall means of exercising market-based “direct democracy”. The customers can pass judgement on an Issuer for practical reasons such as doubt in the reliability of its Credits, or ethical ones, such as the Issuer’s objectionable social and environmental behaviors. 8. Stable. With no no debt owed in anything but product or service, the only cause of Issuer failure is failure to deliver the product or service. There is no structural imperative to continually expand the supply of “money” due to moneylending arithmetic, and no creditors to go bankrupt to except the people holding your Credits. Small losses may be harmlessly absorbed by many Credit holders, all of whom voluntarily acceptedthat Issuer’s Credit. Although expansion is always more enjoyable than contraction, the supply of Producer Credits could just as gracefully contract as expand. There is no built-in growth imperative, and no house of cards to collapse in default, as with the bank credit system. 9. Inclusive. Issuers would not only be made capable of creating enough purchasing power to absorb their own product they would clearly be responsible for doing so. This could lead to the possibility that profit realized by the technological replacement of labor could be used to pay that labor to perform necessary but non-commercial activities, such as environmental cleanup, or any manner of culturally advantageous services. Advances in production techniques could free people to do what they believe in. 10. Abundant. Mortgages would be entirely different. Downturns would be automatically corrected without government intervention. It is amazing what would be possible if the arithmetic were to be reversed. The fundamental difference between the scarcity model and the abundance model is best illustrated by an examination of long term debt, particularly this short chapter on Mortgages. 11. Self-correcting. It would be possible to police the credit issuance of all Issuers to keep it in line with real demand, by a means of an automated market applying a simple formula. |

|

Solution page 8: I assume that if such a system were to be adopted, especially to operate a global network of online automated markets, a network of professional brokerages would be required. In the current system, banks validate the credit worthiness of borrowers, the real money creators. In the proposed system, Producer Credit brokerages would validate the credit worthiness of Producers, the real money creators. Brokerages would validate the Producer Credits validated by other brokerages etc. until an immense global list of validated Producer Credits could be offered to clients. At any time, anyone could single out an Issuer to exclude, for any reason. The brokerage would prosper by ensuring maximum value and security for their clients in exchange for fees. Two simple and obviously fair laws would be required to make brokerages both reliable agents for their clients as well as honest replacements for the current credit rating agencies: 1. Brokers must be paid by BOTH parties to an exchange and; 2. Brokers must be paid in the exact same mix of Credits they have obtained for their clients. Constrained by these two simple rules, brokerages would, in their own self-interest, perform the role ofhonest credit ratings agencies. In the best interests of everyone, brokerages should be numerous, competitive, and in close touch with the Issuers whose Credits they accept and pass on to clients. Brokerages could, for instance, offer insurance in the form of a “guaranteed par” to their clients, taking all the risk and benefits of the Producer Credit system internally. Producer Credits could be issued by any entity in a supply chain, from mines and farms to retail stores. The discount of a primary producer will go to its customer, the next stage processor, and only indirectly into the price the final consumer pays. The final customer may hold the primary producer’s Credit as savings or spend them on something else, but the final customer will never use them to buy directly from the primary producer. Therefore, it would be likely that the major proportion of brokerage functions would happen among distributors, manufacturers, processors, and primary producers. The consumers would only get the producer discount to the extent it might be reflected in the final retail price. Retail entities could also spend Retail Credits as money and offer discounts against redemption in their merchandise exactly as proposed for Producer Credits. Governments would use the exact same concept as well. Government Credits would be spent to provide government services and collected back in resource royalties, user fees and taxes. At the extreme other end of the same proposed system, individuals could use the same value unit and technology to run a local money system entirely on trust between individuals, with their own internal accounting and arrangements and with all credits accepted at par. Using the proposed digital object system, this could be done peer-to-peer, independently and anonymously, in complete isolation from the rest of the system. |

||

|

Solution page 9: The fundamental problem with Producer Credits is the uncertainty of the Issuer’s matching spending with sales. This, of course, is the same problem a business today has borrowing bank credit money to expand its offerings. In the current system, banks are charged with the social role of evaluating who is worthy of credit and of how much. In the proposed system, Credit brokerages would be required to do the same to validate the reliability of Producer Credit Issuers. Existing business-to-business (B2B) and mutual credit systems currently have a variety of ways to evalutate and discipline their Credit Issuers and are actively seeking better means to avoid the misjudgments and attempts at fraud that undermine confidence in the B2B trading system. It is my proposal, that eventually, a computerized marketplace could be developed that could automatically determine, the relative value of any Issuer’s Producer Credits based on the proven demand for that Issuer’s Credits at that moment in time.

The chapter on Self-Correcting System from Money as Debt III In this way Issuers would be disciplined by the market in real time. As would their employees. As well, such a marketplace would yield enormous amounts of anonymous information. All Producer Credits could be evaluated by actual supply and demand without the human intervention of bid/ask as we do now. The volume of buy orders divided by the volume of sell orders results in a ratio which is then multiplied by the value unit. Producer Credit Value = (buy/sell) x Value Unit Given that such an equation for a moment in time could yield results anywhere from zero to infinity, the buy/sell ratio would have to be a moving average over a certain meaningful volume of sales. The design of the moving average would definitely be a job for expert statisticians and the subject of perpetual ongoing refinement. The purpose of the moving average is to eliminate meaningless random variations while reflecting real trends as early as possible. Careful use of this moving average would balance the ability to dampen market volatility with the need for accurate information. This would make it a political issue requiring the setting of recognized standards. |

||

Solution page 10:

Diversity in Money Creation

home / contact

The solution to the problem is to expand the concept of money to include

“promises of something specific from someone specific.”

In the analysis of the problem, I proposed that money, even in the form of gold coins or Bitcoin will eventually concentrate in the ownership of the economically more powerful and become twice-lent. In the current system,where money is created as a debt-of-itself, money is twice-lent by its very nature.

The Standard Theory seems to be that most savings are used for investment. But investment in what? Productive industry that pays wages to people who may have mortgages? Or a money market mutual fund where the money is lent? There’s a big difference. Money invested in productive activity is returned to circulation free of any second debt. It can then be earned by the borrowers who originally created it and paid back to the bank. The debt can be extinguished without creating a new debt. In contrast, money markets, including bank deposits, put a second debt on the same Principal.

Therefore, the proposed solution is that savings be held as redeemable inflation-proofed Producer Credits instead of bank credit. This way, savings are always used to fund short term production.

Savings would be redeemable in real goods and/or services, and retain their purchasing power.

Isn’t that what savings ought to be?

The exchange of conventional money for inflation-proofed Producer Credits would fund Issuers in the conventional money system, while removing the exchange rate and inflation risks for the saver. Most importantly it would return bank credit money to circulation debt-free, relieving the mathematical problem that creates the grow-or-collapse-in defaults imperative in the current scarcity system.

Producer Credits are an expansion of what money means that allows the liberation of money while simultaneously providing the remedy for the current system’s inherent mathematical flaws. Thus the proposed system is put forth as an expansion of banking because there is no need to do away with banking.

This could be a cooperative transition.

To illustrate, please consider this spectrum of payment methods.

|

Solution page 11: The solution is to create and combine different ways to create money

Currently the only way to create money is to get into debt to a bank. And repayment is in money only.

The solution is to expand beyond that paradigm, and also use as money, reliable promises of products or services denominated in an inflation-proofed value unit, the Producer Credit as previously described. This provides a second way to create money, as debt payable in goods and/or services only, with a value unit that defines its value in terms of a basket of global commodities.

And add to that, Time Money which is denominated only in hours. Time Money is like Producer Credits, a promise of something specific from someone specific. Any kind of exchange can be reckoned in hours and at any rate of exchange the participants agree upon. If you do something for someone else who is willing to pledge their future time in exchange, then you have created “money” that you can spend on someone else’s time. All value exchanges are subjective and voluntary. Participants are made aware of the local minimum wage for personal comparison purposes only.

And lastly, I propose a means of facilitating Gifting which can take any form. Gifts can be requested. And giving can be recorded as “social capital” if that is the donor’s wish. All of these modes of exchange currently exist, and have throughout human history. The solution is to make them interchangeable so that theoretically a gift could be exchanged for Time Money which could be traded for Producer Credits, then exchanged for bank credit and paid out in fiat cash all within the same account within the Payment Spectrum. In addition to the gifting module, such a brokerage could also offer community networking, employment and sales services that allow account holders to advertise their goods and services to each other and build “tribes” of people who interact with each other using all 4 modes of exchange. |

||

|

Solution page 12: What is being proposed here, in detail, is a whole new inclusive and self-balancing economic system. Money as Debt III – Evolution Beyond Money The proposed solution is to expand what it means to be a bank. Below is a Flash mockup I made of a Payment Spectrum user interface, complete with details, demos and “user stories”. |

||

|

Solution page 13: The current money system has long been noted for the many ways it can be “gamed”, through criminal acts or legally. These crimes and abuses of the public good have been recognized by a substantial portion of the public now that income disparity and financial crime has been highlighted by the Crash of 2008, the Occupy Movement and similar uprisings worldwide.

How would the same criminally inclined persons pull a fast one in the Producer Credit system? Several people have insisted that ANY system can be gamed. I have repeatedly invited them to submit their ideas of how the Producer Credit system could be manipulated to someone’s unfair advantage, both within the rules and in violation of them. That invitation is still OPEN. There has been only one rather obvious suggestion so far, from multiple sources: The Issuer Spends Credits and then Closes Shop Producer Credits aren’t anonymous like cash in a vault that can be stolen or a Swiss bank account that can be emptied. Producer Credits can only be created by the Issuer, in most cases the company, spending them on something. This expenditure would show up in the records immediately. And, everything bought would be traceable the moment it was bought. But, assuming the owner, the financial officer and bookkeeper all make their escape, the company closes and the Issuer’s Producer Credits fall to zero value, the situation is exactly the same as covered under the page onLosses in general. Fly-by-night operations spending fraudulent Producer Credits and then disappearing would rob whoever is holding their Credits just as with fake securities now. But how could that happen? It couldn’t. It would take a record of dependable performance to establish that sort of volume of credit within the Producer Credit system. Only a desperate Issuer would throw that away. Systemic Collapse? Other Possibilities Counterfeiting General Devaluation Given that devalued credit must be guaranteed by the Issuer to be redeemed at par, and over-valued Credits would create a shortage of product as well as hand the Issuer’s profits to its customers, there would never be any advantage to an Issuer in deliberately devaluing or overvaluing its Credits. To be perceived by the public as a devaluing credit that will not recover its value would be the kiss-of-death to an Issuer. The Issuer would be at the mercy of currency speculators or a fire-sale takeover. Remaining at par or very slightly above would always be the goal of a Issuer that wanted to stay in business. Hostile Takeover If Aggressor Corp. buys up a huge amount of Competitor X Credits, it could withhold the Competitor X Credits as they near maturity, and drive up the value so that Competitor X loses all of its projected profits to its customers because they are redeeming Producer Credits at far in excess of par. Competitor X is, therefore, also running out of stock before all the Competitor X Producer Credits issued against that stock are redeemed, and is thus at risk of default. Then, at the last minute, just before the Competitor X Credits expire, Aggressor Corp. demands redemption in a huge amount of product. Competitor X can’t redeem its Credits on time and is now legally at the mercy of Aggressor Corp. The Defense is Simple More immediately redeemable Competitor X Credits would bring the Competitor X Credits value back to par. If Aggressor Corp. now offers its excess Competitor X Credits on the market, their value will plummet well below par and be very close to expiring. Aggressor Corp. now has three choices: 1. take a total loss, or; 2. sell the Competitor X Credits to third parties, probably at a loss; 3. accept payment from Competitor X in the other Producer Credits Competitor X acquired or; 4. insist on redeeming the Competitor X Credits for Competitor X product. In the first case, the Aggressor Corp. takes a loss in order to push Competitor X Credits below par and try to start a run on the company’s Credits. However, Competitor X has other Producer Credits, presumably at par, with which Competitor X buys up its excess Credits, nullifying the attack. Not only is Aggressor Corp. foiled, butAggressor Corp.’s loss is Competitor X’s profit! In the second and third cases, Aggressor Corp.’s attack is turned back and nullified. In the fourth case, Competitor X is capable of paying for the required production with the Credits of the other Producers it bought to defend itself. Buying the necessary time might require a decision by a court. If this system were the prevailing system, the legal procedures for this situation would be well mapped out and probably require rigidly arbitrated settlements to save court costs. In the case of obvious aggression, why would the rules favour the aggressor? Given these outcomes, such aggression via currency manipulation does not seem promising. Self-destruction more Credible Currency Speculators In the case of a loss of reputation, discerning whether a company’s real demand will survive an attack on its reputation would be the role of the currency speculators. In their own best interest, currency speculators would have to exercise due diligence and sound evaluation of credit risk. Such due diligence would be a public service rendered for profit by private interests at their own risk, not a government bureaucracy.

The Section of Money as Debt III on Devaluation & Speculation Brokers and Speculators The rules of this system must stipulate that brokers get paid their fees by both sides of each transaction, in the exact same mix of Producer Credits they transact for their clients. These are clear and common sense rules that would keep brokers honest and effectively provide a functional replacement for credit rating agencies. The big question that would repeatedly come up would be… should Producer Credit brokerages be allowed to speculate in Producer Credits for their own profit? Given that brokers could influence the swings in value, NO. Potential conflict-of-interest could only be avoided if brokerages and speculators were strictly separated. In addition, this would make the speculators’ assessment of the credit risk of any Issuer independent of the brokerages’ assessments, an additional pressure to keep Issuers and brokerages honest and factual. |

||