Game theory—in practice

February 17, 2015

from David Ruccio

Back when I taught Principles of Microeconomics, I offered a lecture or two on game theory. Given how terrible most textbook presentations are, I used to borrowed heavily from the work of Judith Mehta and Shaun Hargreaves-Heap and Yanis Varoufakis to explain the key assumptions behind and the tensions generated within game theory.

Now, Varoufakis is back—in a very different capacity, of course—to explain the lesson he learned from his studies of game theory:

The trouble with game theory, as I used to tell my students, is that it takes for granted the players’ motives. In poker or blackjack this assumption is unproblematic. But in the current deliberations between our European partners and Greece’s new government, the whole point is to forge new motives. To fashion a fresh mind-set that transcends national divides, dissolves the creditor-debtor distinction in favor of a pan-European perspective, and places the common European good above petty politics, dogma that proves toxic if universalized, and an us-versus-them mind-set.

And the payoff?

One may think that this retreat from game theory is motivated by some radical-left agenda. Not so. The major influence here is Immanuel Kant, the German philosopher who taught us that the rational and the free escape the empire of expediency by doing what is right.

How do we know that our modest policy agenda, which constitutes our red line, is right in Kant’s terms? We know by looking into the eyes of the hungry in the streets of our cities or contemplating our stressed middle class, or considering the interests of hard-working people in every European village and city within our monetary union. After all, Europe will only regain its soul when it regains the people’s trust by putting their interests center-stage.

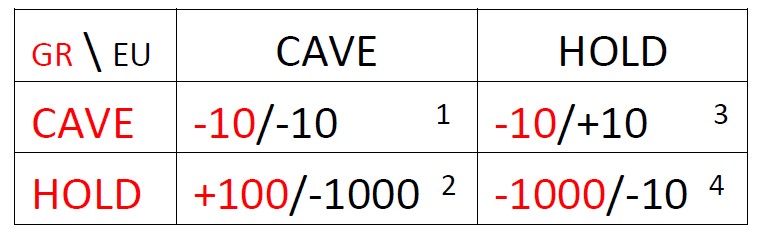

*This is Bill O’Grady’s view of the payoff matrix of the “game” being played by Greece and the EU—as seen by the Syriza party.

Our view is that Syriza believes that caving in to the EU will end its political movement before it really begins. Caving in produces the outcome of -100 in quadrants one and three. Thus, its only positive payoff is to press for restructuring at all costs, while the EU caves (quadrant two outcome). At the same time, we think Tsipras believes that the costs to the EU of caving to Syriza aren’t all that high, but a situation in which both parties hold (quadrant four outcome), which probably entails a Greek exit from the Eurozone, is devastating for the EU. If the Eurozone breaks up, the Pandora Media Inc (NYSE:P)’s Box of European nationalism is released with all the risks that entails. The conditions that led to two world wars will return. And, most importantly, Germany loses its single currency free-trade zone. Thus, we fear that Syriza has concluded that the EU/Germany/ECB has no choice but to cave as long as Syriza holds firm.

Greece does battle with creationist economics: can Germany be brought into the 21st Century?

from Dean Baker

Europeans have been amused in recent weeks by the difficulty that Republican presidential candidates have with the theory of evolution. But these cognitive problems will only matter if one of these people gets into the White House and still finds himself unable to distinguish myth from reality. By contrast, Europe is already suffering enormous pain because the people setting economic policy prefer morality tales to economic reality.

This is the story of the confrontation between Greece and the leadership of the European Union. The northern European countries, most importantly Germany, insist on punishing Greece as a profligate spender. They insist on massive debt payments from Greece to the European Union and other official creditors to make up for excessive borrowing in prior years.

The current program requires that Greece’s tax revenues exceed non-interest government spending by 4.0 percent of GDP, the equivalent of $720 billion a year in the United States. This money is pulled out of Greece’s economy and sent to its creditors. Making matters worse, because Greece is locked into the euro at present, it is not able to regain competitiveness by lowering the value of its currency relative to the richer countries in Europe.

The result of the German program for Greece has been an economic downturn that makes the Great Depression in the United States look like a bad day. Seven years after the start of the downturn Greece’s economy is more than 23 percent smaller than its peak in 2007.

By comparison, at the trough of the Great Depression in 1933 the U.S. economy was 26 percent below its pre-recession peak in 1929, but it grew 10 percent the following year and had made up all the lost ground by 1936. On its current path Greece will be lucky if it returns to its pre-crash GDP by the middle of the next decade, twenty years after the crash.

The tales of hardship are endless: an unemployment rate of more than 25 percent, a youth unemployment rate of more than 50 percent, a collapsed health care system. The European Union folks may not know much economics, but they sure know how to destroy a country.

Interestingly, even their morality tale is at best half-true. Greece was a profligate spender, but what about punishing the reckless lenders? They were largely bailed out by the European Union, the International Monetary Fund and the European Central Bank, who now hold the vast majority of Greek debt. What about punishing Goldman Sachs, which designed the swap that allowed Greece to hide its debt so it could get into the euro in the first place?

Apparently the desire to punish sin only applies to the weak, not the rich and powerful who commit transgressions. The double standard is even clearer when applied to crisis countries like Spain and Ireland who had not been profligate borrowers. They had been running budget surpluses before the crisis. This was entirely a story of reckless lenders in Germany and elsewhere making bad loans to the private sector in these countries. Yet, the austerity policies being imposed ensure that the people of Spain and Ireland suffer even if the pain is not quite bad as in Greece.

The absurdity is that if the northern Europeans could get over their need to inflict pain, it would be easy to design policies which would allow the whole continent to benefit from more growth. If the deficit target for Greece was relaxed, it would be able to grow more rapidly. For example, assuming a multiplier of 1.5 (GDP grows one and a half times any increase in government spending), if Greece was required to run a primary budget surplus of 1.0 percent of GDP rather than 4.0 percent of GDP, its GDP could expand by 4.5 percent due to additional government spending. In fact, since the additional growth would lead to additional tax revenue, Greece’s economy would likely expand by more than 6.0 percent with this lower target.

The obvious complaint from the northern countries is that if Greece gets this concession other crisis countries will demand the same. That is correct, and they should get similar relief. The net effect will be much stronger growth in southern Europe, which will lead to increased demand and more growth in northern Europe as well. What exactly is the problem?

Since the crash, which incredibly caught all the economic “experts” by surprise, we have seen one myth after another destroyed by the evidence. Deficit reduction did not lead to a surge in investment due to increased confidence. Printing money in a badly depressed economy did not lead to runaway inflation or plunging currency values.

The time has come for the European Union to stop running economic policy based on silly myths. If German Chancellor Angela Merkel and other leaders in the European Union cannot accept reality then Greece and southern Europe would be far better off breaking free of the euro and leave Germany to wallow in its 19th century economic fairy tales.

Reforms in Greece. An exemplary record. But the wrong track. 3 graphs.

Greece is champion reformer. According to austerity mythology, we did not have a financial but a ‘rigidity’ crisis, aggravated by uncompetitive price levels. Which had to be solved with structural reforms and by bringing the price level (read: wages) down. Which is what Greece did, much more than any other country. But, as we do not have a rigidity crisis but a monetary crisis this did not work, of course. Some data: via Frances Coppola we learn that Greece has been the most ardent reformer of the entire Eurozone (graph 1, OECD data). Via Paul Krugman we learn that no country cut government expenditure as much as Greece (by a long shot: graph 2, Eurostat data). And Eurostat also teaches us that no country has been as succesful as Greece in lowering relative and even absolute prices (graph 3, Eurostat data). Coppola and Krugman are, understandable, aghast about the hypocrisy of the prime ministers of Ireland and Finland, who are lecturing Greece about something which it did much more succesfully than they did. And then there is the argument: “the Irish suffered for nothing, so the Greek have to suffer too“. Sigh.

Remark: the Krugman graph jpg has a lot of white below the actual graph.

Graph 1. OECD shows that Greece did reform

Graph 2. Krugman shows that Greece did cut government expenditure

Graph 3. Price data shows that the Greek relative price level declined much more than the Irish or the Baltic one

Share this:

Greek retreat from game theory

from Lars Syll

ATHENS — I am writing this piece on the margins of a crucial negotiation with my country’s creditors — a negotiation the result of which may mark a generation, and even prove a turning point for Europe’s unfolding experiment with monetary union.

Game theorists analyze negotiations as if they were split-a-pie games involving selfish players. Because I spent many years during my previous life as an academic researching game theory, some commentators rushed to presume that as Greece’s new finance minister I was busily devising bluffs, stratagems and outside options, struggling to improve upon a weak hand.

Nothing could be further from the truth.

If anything, my game-theory background convinced me that it would be pure folly to think of the current deliberations between Greece and our partners as a bargaining game to be won or lost via bluffs and tactical subterfuge.

The trouble with game theory, as I used to tell my students, is that it takes for granted the players’ motives. In poker or blackjack this assumption is unproblematic. But in the current deliberations between our European partners and Greece’s new government, the whole point is to forge new motives. To fashion a fresh mind-set that transcends national divides, dissolves the creditor-debtor distinction in favor of a pan-European perspective, and places the common European good above petty politics, dogma that proves toxic if universalized, and an us-versus-them mind-set.

As finance minister of a small, fiscally stressed nation lacking its own central bank and seen by many of our partners as a problem debtor, I am convinced that we have one option only: to shun any temptation to treat this pivotal moment as an experiment in strategizing and, instead, to present honestly the facts concerning Greece’s social economy, table our proposals for regrowing Greece, explain why these are in Europe’s interest, and reveal the red lines beyond which logic and duty prevent us from going.

The great difference between this government and previous Greek governments is twofold: We are determined to clash with mighty vested interests in order to reboot Greece and gain our partners’ trust. We are also determined not to be treated as a debt colony that should suffer what it must. The principle of the greatest austerity for the most depressed economy would be quaint if it did not cause so much unnecessary suffering.

I am often asked: What if the only way you can secure funding is to cross your red lines and accept measures that you consider to be part of the problem, rather than of its solution? Faithful to the principle that I have no right to bluff, my answer is: The lines that we have presented as red will not be crossed. Otherwise, they would not be truly red, but merely a bluff.

But what if this brings your people much pain? I am asked. Surely you must be bluffing.

The problem with this line of argument is that it presumes, along with game theory, that we live in a tyranny of consequences. That there are no circumstances when we must do what is right not as a strategy but simply because it is … right.

Against such cynicism the new Greek government will innovate. We shall desist, whatever the consequences, from deals that are wrong for Greece and wrong for Europe. The “extend and pretend” game that began after Greece’s public debt became unserviceable in 2010 will end. No more loans — not until we have a credible plan for growing the economy in order to repay those loans, help the middle class get back on its feet and address the hideous humanitarian crisis. No more “reform” programs that target poor pensioners and family-owned pharmacies while leaving large-scale corruption untouched.

Our government is not asking our partners for a way out of repaying our debts. We are asking for a few months of financial stability that will allow us to embark upon the task of reforms that the broad Greek population can own and support, so we can bring back growth and end our inability to pay our dues.

One may think that this retreat from game theory is motivated by some radical-left agenda. Not so. The major influence here is Immanuel Kant, the German philosopher who taught us that the rational and the free escape the empire of expediency by doing what is right.

How do we know that our modest policy agenda, which constitutes our red line, is right in Kant’s terms? We know by looking into the eyes of the hungry in the streets of our cities or contemplating our stressed middle class, or considering the interests of hard-working people in every European village and city within our monetary union. After all, Europe will only regain its soul when it regains the people’s trust by putting their interests center-stage.

Varoufakis’ retreat from game theory is a perfect illustration of the limitations of überrationalistic modeling and what happens when confronting deductive-axiomatic economic models with reality.

Back in 1991, when yours truly earned his first Ph.D. with a dissertation on decision making and rationality in social choice theory and game theory, I concluded that “repeatedly it seems as though mathematical tractability and elegance — rather than realism and relevance — have been the most applied guidelines for the behavioural assumptions being made. On a political and social level it is doubtful if the methodological individualism, ahistoricity and formalism they are advocating are especially valid.”

This, of course, was like swearing in church. My mainstream neoclassical colleagues were — to say the least — not exactly überjoyed.

For those of you who are not familiar with game theory, but eager to learn something relevant about it, I have three suggestions:

Start with the best introduction there is

and then go on to read more on the objections that can be raised against game theory and its underlying assumptions on e.g. rationality, “backward induction” and “common knowledge” in

and then finish off with listening to what one of the world’s most renowned game theorists — Ariel Rubinstein — has to say on the — rather limited — applicability of game theory in this interview (emphasis added):

What are the applications of game theory for real life?

That’s a central question: Is game theory useful in a concrete sense or not? Game theory is an area of economics that has enjoyed fantastic public relations. [John] Von Neumann [one of the founders of game theory] was not only a genius in mathematics, he was also a genius in public relations. The choice of the name “theory of games” was brilliant as a marketing device.

The word “game” has friendly, enjoyable associations. It gives a good feeling to people. It reminds us of our childhood, of chess and checkers, of children’s games. The associations are very light, not heavy, even though you may be trying to deal with issues like nuclear deterrence. I think it’s a very tempting idea for people, that they can take something simple and apply it to situations that are very complicated, like the economic crisis or nuclear deterrence. But this is an illusion. Now my views, I have to say, are extreme compared to many of my colleagues. I believe that game theory is very interesting. I’ve spent a lot of my life thinking about it, but I don’t respect the claims that it has direct applications.

The analogy I sometimes give is from logic. Logic is a very interesting field in philosophy, or in mathematics. But I don’t think anybody has the illusion that logic helps people to be better performers in life. A good judge does not need to know logic. It may turn out to be useful – logic was useful in the development of the computer sciences, for example – but it’s not directly practical in the sense of helping you figure out how best to behave tomorrow, say in a debate with friends, or when analysing data that you get as a judge or a citizen or as a scientist.

…

In game theory, what we’re doing is saying, “Let’s try to abstract our thinking about strategic situations.” Game theorists are very good at abstracting some very complicated situations and putting some elements of the situations into a formal model. In general, my view about formal models is that a model is a fable. Game theory is about a collection of fables. Are fables useful or not? In some sense, you can say that they are useful, because good fables can give you some new insight into the world and allow you to think about a situation differently. But fables are not useful in the sense of giving you advice about what to do tomorrow, or how to reach an agreement between the West and Iran. The same is true about game theory.

…

In general, I would say there were too many claims made by game theoreticians about its relevance. Every book of game theory starts with “Game theory is very relevant to everything that you can imagine, and probably many things that you can’t imagine.” In my opinion that’s just a marketing device.

Why do it then?

… What I’m opposing is the approach that says, in a practical situation, “OK, there are some very clever game theoreticians in the world, let’s ask them what to do.” I have not seen, in all my life, a single example where a game theorist could give advice, based on the theory, which was more useful than that of the layman.

…

Looking at the flipside, was there ever a situation in which you were pleasantly surprised at what game theory was able to deliver?

None. Not only none, but my point would be that categorically game theory cannot do it.

One of the proof methods that I was especially critical of in my dissertation was the use of “backward induction.” I have to confess I haven’t given it much thought outside the class room since then, but after having spent yesterday afternoon reading Ken Binmore’s Game Theory: A Very Short Introduction, I have to confess I’m slightly surprised that it — obviously — still holds such a strong position among game theorists. For those of you not familiar with it I recommend looking at the video below and afterwards take a minute or two and try to figure out how convinced you are about backward induction really helping us to understand what is after all the very idea of game theory — to analyze, understand, and explain strategic thinking …